Digital Payments in India

From being majorly a cash-obsessed economy, India’s digital payments journey is a new and budding story. Driven by progressive regulatory policies and increased use of mobile internet, Indian payment industry is going through a transformational phase. The next few years will witness a whole new way of how money is moved in the Indian economy.

The exponential growth of the digital payments sector is driven by multiple factors including convenience to pay, smartphone penetration, rise of non-banking payment institutions (payments bank and digital wallets), progressive regulatory policies, improvement of the digital infrastructure and increasing consumer readiness to the digital payment platform.

Another key driver of digital payments is positive policy framework changes and government initiatives like launch of new digital payments systems like – IMPS, UPI and BHIM.

IMPS:

Immediate Payment Service (IMPS) is an instant, real-time, inter-bank, electronic funds transfer system in India. Unlike NEFT and RTGS, the service is available 24/7 throughout the year including bank holidays.

It is managed by the National Payments Corporation of India (NPCI) and is built upon the existing National Financial Switch network. In 2010, the NPCI initially carried out a pilot for the mobile payment system with 4 member banks (State Bank of India, Bank of India, Union Bank of India and ICICI Bank), and expanded it to include Yes Bank, Axis Bank and HDFC Bank later that year. IMPS was publicly launched on November 22, 2010. Currently, there are 53 commercial banks, 101 Rural/District/Urban and cooperative banks, and 24 PPIi (private placement life insurance) signed up for the IMPS service.

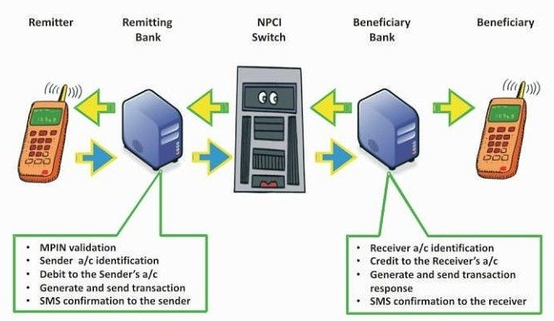

IMPS transaction flow:

- Remitter sends instruction from his/her mobile through his/her bank provided application or SMS.

- Remitting bank validates the details of the remitter and debits his/ her account. This transaction is sent by the remitting bank to NPCI.

- Transaction is passed by NPCI to the beneficiary bank. Beneficiary Bank validates the details of the beneficiary customer, credits the account, sends confirmation to NPCI about transaction status and sends a sms to the beneficiary customer informing him of the credit.

- NPCI sends the transaction status to remitting bank which in turn informs the status of the transaction to the Remitter.

- Remitting bank send a sms confirmation of the transaction to the remitting customer.

UPI:

Unified Payments Interface (UPI) is an instant real-time payment system developed by National Payments Corporation of India facilitating inter-bank transactions. The interface is regulated by the Reserve Bank of India and works by instantly transferring funds between two bank accounts on a mobile platform.

Even after introducing net-banking in India, the number of cash transaction happening in India is very high (almost 95% of all transactions). UPI is part of RBI’s efforts towards ‘Less Cash’ India. It is standardized across banks, which means you can initiate a bank account transfer from anywhere with a few clicks. This means that UPI will help you to pay directly from your bank account to different merchants without the hassle of typing your netbanking password, credit card details or IFSC code. Apart from cards, netbanking and wallets, your can now pay through UPI too. Unified Payment Interface (UPI) allows to pay someone as well as ‘collect’ cash from someone.

After demonetization in November 2016, there was a major boost in the use of digital payment methods in India. According to the NPCI, the value of the UPI transactions skyrocketed to INR 1 Tn while the volume of transactions reached 913 Mn, up from 7 Mn in April 2017.

UPI is built over Immediate Payment Service (IMPS) for transferring funds. Being a digital payment system it is available 24*7 and across public holidays. Unlike traditional mobile wallets, which takes a specified amount of money from user and stores it in its own accounts, UPI withdraws and deposits funds directly from the bank account whenever a transaction is requested. It uses Virtual Payment Address Account Number with IFS Code, Mobile Number with MMID, Aadhaar Number, or a one-time use Virtual ID. An MPIN (Mobile banking Personal Identification number) is required to confirm each payment.

6 Steps to start using UPI

- Check if your bank has released an updated mobile app with UPI support already.

- Download the UPI app of your bank from Google Play Store/Apple Apps Store

- Set app login.

- Create a Virtual Payment Address (VPA). Eg: trenovision@axis

- Add your bank account.

- Set MPIN.

- Start transacting using UPI.

For example, consider that you are trying to book tickets online for a film via your mobile. When you click buy, the mobile website/ mobile app you used will trigger the UPI payment link. Now, you are taken to the pay screen of the UPI app. Here, the transaction information is verified and a click followed by entry of a secure PIN completes the purchase.

How safe is UPI?

- UPI offers better security than other payment methods where details like credit card numbers are send. While using UPI, all these details are hidden as only a Virtual Payment Address (VPA) is used and no other sensitive information is shared.

- The virtual payment address does not allow your security to be compromised even when a certain merchant’s account is hacked, because their database will have only a list of virtual addresses. The payment addresses are denoted by ‘account@payment_service_provider’.

BHIM:

BHIM (Bharat Interface for Money) is a mobile app developed by National Payments Corporation of India (NPCI), based on the Unified Payment Interface (UPI). It was launched by Narendra Modi, the Prime Minister of India, at a Digi Dhan mela at Talkatora Stadium in New Delhi on 30 December 2016. It was named after Dr. Bhimrao R. Ambedkar and is intended to facilitate e-payments directly through banks as part of the 2016 Indian banknote demonetisation and drive towards cashless transactions.

BHIM supports all Indian banks which use that platform, which is built over the Immediate Payment Service infrastructure and allows the user to instantly transfer money between bank accounts of any two parties. It can be used on all mobile devices.

BHIM users can send money by knowing the following details of the receiver:

- UPI ID ( Registered on UPI)

- Mobile No. (Registered on BHIM or *99#)

- Account no. & IFS Code

- Aadhaar Number

There is a Rs. 10,000 per transaction limit, and Rs. 20,000 per day for BHIM.

The following are the features of BHIM:

- Send Money: Send money by entering Virtual Payment Address (UPI ID), Account number and QR Scan.

- Request Money: Collect money by entering Virtual Payment Address (UPI ID). Additionally through BHIM App, one can also transfer money using Mobile No. (Mobile No should be registered with BHIM or *99# and account should be linked).

- Scan & Pay: Pay by scanning the QR code through Scan & Pay or generate your to let others make easy payments to you.

- Transactions: Check your transaction history and also pending UPI collect requests (if any) You can raise complaint for the declined transactions by clicking on report issue in transactions.

- Profile: You can view the static QR code and Payment addresses linked to your account. You can also share the QR code through various messenger applications like WhatsApp, Email etc. available on phone and can also download the QR code.

- Bank Account: Switch between multiple bank accounts linked with your BHIM App. You can set/change your UPI PIN or check your balance.

- Language: Currently BHIM is available in 12 languages, i.e., Hindi, English, Tamil, Telugu, Malayalam, Bengali, Odia, Kannada, Gujarati, Marathi, Assamese and Bengali.

- Block User: Block/Spam users who are sending you collect requests from illicit sources.

- Privacy: Allow a user to disable and enable mobilenumber@upi in the profile if a secondary UPI ID is created (QR for the disabled UPI ID is also disabled).

- Payment Reminders: Schedule payments as per your convenience.

- Split Bill: Splitting bills with multiple UPI users at a click of a button.

Benefits of using of BHIM App:

- The app allows you to easily transfer money or make a payment from your bank account using only your phone number.

- You just need to open the app, choose “send money”, and type in the amount and the merchant’s phone number to make the payment. The money will be debited from your account, and credited to the merchant’s bank account which are linked by you and the vendor to the BHIM app.

- The app also allows you to scan a QR code. The merchant can generate his QR code through the BHIM app. To pay him, you’d need to tap the Scan and Pay button in the app, and then scan the QR code.

- Even without a Smartphone, anyone can use BHIM to make payments. You need to dial *99# from any kind of mobile phone, and this will show a menu – by typing in different numbers you can choose to send money, check your balance, or see transaction history. To send money, for example, you’d type ‘1’ and hit send, then type ‘1’ again to select mobile number. Next, you’d type in the number and the amount, and then a PIN that can be generated using BHIM. This will work on any phone without an Internet connection.

- With a mobile wallet app, you have to load money in the wallet before you can use it. With BHIM and all UPI apps, you can directly connect your phone to your bank account – like a debit card. Payments are happening directly from and to bank accounts, so merchants don’t have to worry about transferring wallet earnings to the bank either.

- All UPI-connected banks accept BHIM – this includes all major Indian banks including SBI, ICICI, Axis, and HDFC. Even banks not connected to UPI can receive money through BHIM through IFSC code.

Current Challenges and Growth Prospects:

- The Indian economy continues to be heavily reliant on cash.

- Digital payment systems are heavily reliant on smartphones as they require data connections, NFC and bluetooth etc. Out of India’s 800 Mn mobile phone users, only 200 Mn use smartphones, only 6 Mn of which are NFC-enabled. An even smaller percentage of users has access to QR code mechanisms. This means approximately 85% Indians do not have access to the infrastructure required to adopt the current digital payment systems. There is a dire need, therefore, for a more interoperable and universal method of digital payments in the country.

- The solutions available now are catering to individuals who are already well versed with cashless transactions through credit/debit cards and net banking.